Key Takeaways

- “Best value” means total project cost, budget predictability, and timeline risk—not just the contract price.

- Semi-custom homes offer fixed pricing based on actual material selections; custom builds often rely on allowances that shift the final cost.

- Semi-custom builds typically complete in 7–8 months; custom builds take 10–13 months—and every extra month costs real money.

- Reinbrecht Homes offers free construction financing up to $250,000 with as little as $1,000 down—eliminating interest-only payments during the build.

- Use the Value Scorecard and Decision Checklist below to match the right build type to your priorities.

If you’re weighing the cost of a semi-custom home against a fully custom build, the answer probably isn’t what you expect. The cheapest option on paper is rarely the cheapest in practice. True value depends on what you actually spend, how long the process takes, how predictable the budget stays, and how well the finished home holds its worth over time.

This guide breaks down every cost factor that separates the two build types so you can make a confident decision. Whether you’re building in one of Reinbrecht Homes’ neighborhoods or on your own lot, this framework will help you find the path that delivers the most home for your money.

“Best Value” Doesn’t Mean “Lowest Price”—Here’s What It Really Means

When most buyers compare costs, they focus on the base contract price. That number matters, but the real measure of value accounts for every dollar from first meeting to move-in day.

Total Project Cost vs. Base Price

Base price is what shows up on a contract. Total project cost adds everything else:

- Architecture and design fees

- Permit and impact fees

- Site preparation and utility connections

- Every upgrade and change order

- Temporary housing if the build runs long

- Closing costs tied to your financing structure

A semi-custom home typically folds most of these into a single transparent number. A custom home often starts with a lower “structure-only” estimate that grows as design and site work layers on.

Budget Predictability as a Cost

When a project relies on allowances—placeholder dollar amounts for finishes not yet selected—the final number can swing significantly. Reinbrecht Homes eliminates allowances on semi-custom builds by having buyers select actual materials upfront, so the price you sign is the price you pay. As one homeowner put it: “They do this amazing price lock, the price you sign is the price you pay!”

Timeline Cost (Temporary Housing, Rate-Lock Risk)

Every month past the expected completion date costs real money—rent on temporary housing and potential rate-lock expiration that could raise your interest rate for 30 years. Timeline risk affects custom builds far more than semi-custom ones because there are more variables in play.

Quick Definitions (Apples to Apples)

Before comparing costs, it helps to define exactly what each build type involves.

What Is a Semi-Custom Home?

A semi-custom home starts with a pre-designed floor plan. You choose the plan that fits your needs, then customize selections—paint, cabinets, flooring, countertops, siding, fixtures, and more. At Reinbrecht Homes, buyers choose from 30+ customizable floor plans with standard features covering every component from driveway to roof. Pre-construction takes about one month and construction about six months—move-in ready in as little as seven months.

What Is a Fully Custom Home?

A fully custom home is designed from scratch—you and your builder (and often your own architect) determine every detail. At Reinbrecht Homes, the custom home process involves a pre-construction phase of two to three months and a construction phase of eight to ten months.

Why Two “Similar” Homes Can Cost Wildly Different Amounts

Two 2,200-square-foot homes can differ by tens of thousands of dollars. The custom version may require original drawings, structural engineering, multiple revisions, and specialty sourcing. The semi-custom version uses a proven plan with pre-negotiated pricing. They may look comparable from the street, but the cost of the path to get there can be vastly different.

The Real Cost Drivers: Where Semi-Custom and Custom Diverge

These are the categories where the two build types produce the biggest financial gaps.

Plans, Architecture, and Redraw Cycles

Semi-custom plans already exist, have been built before, and are priced accurately. Reinbrecht can price one in as little as an hour. Custom homes require original plans that almost always go through multiple revision cycles—each adding fees and weeks. A custom home typically requires several meetings, architect visits, and weeks to finalize plans plus additional time to calculate the final price.

Structural Changes vs. Finish Selections

Semi-custom builds focus decisions on finish selections that personalize the home without altering its structure. Custom builds open the door to structural changes that ripple through multiple trades:

- Engineering and architectural revisions

- Framing modifications

- HVAC routing changes

- Plumbing and electrical rework

Every structural change cascades through each of these areas, and each carries a cost.

Selections Complexity (Decision Volume)

Reinbrecht streamlines semi-custom choices with curated selections—six preselected door styles instead of a 300-page catalog, per their Semi-Custom Standards Guide. You still get variety (14 countertop styles, 10 carpet styles, 14 LVT wood looks) without the paralysis of unlimited options. On a custom build, you select every detail from scratch—more freedom, but significantly more decisions and more opportunity for cost overruns.

Change Orders and Rework (The Silent Budget Killer)

Change orders—modifications after the contract is signed—are far more common on custom builds. Each typically carries markups for:

- Administrative and re-engineering costs

- Material swaps or reorders

- Schedule disruption and labor rework

Semi-custom builds minimize change orders because plans are proven, materials are selected upfront, and the builder has deep experience executing each design.

Semi-Custom vs. Custom “Value Scorecard”

Compare the two build types across the factors that most directly affect your total investment.

| Factor | Semi-Custom | Custom |

| Upfront Cost Transparency | High – Straight costs with no allowances; price at signing is the final price | Moderate – Allowances common; final cost unknown until all selections complete |

| Cost Certainty | Fixed contract price based on actual material selections | Variable – Allowances and change orders can shift the final number significantly |

| Timeline | ~7 months total (1 mo. pre-construction + 6 mo. build) | ~10–13 months total (2–3 mo. pre-construction + 8–10 mo. build) |

| Customization | High within proven plan framework; layout, finishes, and features all customizable | Unlimited – Every detail designed from scratch |

| Financing | Simpler – Free construction financing up to $250K, $1,000 down, zero interest during build | More complex – Traditional construction loan with draws, inspections, interest-only payments |

| Appraisal Risk | Lower – Proven plans with comparable sales data available | Higher – Unique designs harder to appraise; may affect loan amounts |

| Resale Fit | Strong – Broad market appeal with personal touches | Varies – Highly personalized designs may narrow buyer pool |

A few factors worth highlighting: Reinbrecht’s “straight costs” approach means buyers choose from actual material samples rather than estimated allowances—so the contract price is based on real numbers, not placeholders. Instead of offering an allowance of $2,000 for flooring, they sit down with you to select the exact product and determine the exact cost. No surprises at closing.

On the financing side, Reinbrecht offers free construction financing up to $250,000 with as little as $1,000 down and zero interest-only payments during the build. Traditional custom construction loans typically require draw schedules, periodic lender inspections, and monthly interest payments throughout—all of which add cost and complexity. For appraisal risk, semi-custom homes built from popular floor plans tend to appraise smoothly because comparable sales data is readily available. Unique custom designs can be harder for appraisers to value, occasionally creating a financing gap the buyer must cover out of pocket.

When Semi-Custom Is the Best Value

For the majority of buyers, semi-custom hits the sweet spot between personalization and predictability.

Personalization, Not Unlimited Design

Most buyers don’t need to design from scratch—they need a home that fits their lifestyle with the finishes they love. You choose a floor plan that matches your needs, then personalize it with your preferred materials, colors, and upgrades. Structural modifications like shifting walls or adjusting room sizes are often possible within the builder’s framework. The result is a home that feels uniquely yours without the cost and time required for full architectural design.

Fewer Change Orders, Less Decision Fatigue

Proven plans with curated material options mean fewer mid-build changes. You make selections before construction begins—fewer surprises, less stress, and a more predictable budget.

Faster Move-In, Better Budget Control

Move-in ready in as little as seven months. Combined with free construction financing and upfront pricing, the shorter timeline means less rate-lock risk, less temporary housing cost, and a faster return on your investment.

When Custom Is Worth the Extra Cost

Custom costs more, but for some buyers it’s the only path that makes sense. The key is knowing whether your situation genuinely calls for a ground-up design.

Unique Lot or Specialty Needs

If your lot has unusual topography, setback requirements, or orientation challenges, a pre-designed plan may not work. Reinbrecht builds both custom and semi-custom homes on your own lot or in their neighborhoods—either path is available depending on site conditions.

One-of-One Design Requirements

Some visions—a specific roofline, a multi-generational suite with separate entrances, an integrated workshop—simply can’t be achieved within existing plans. For these buyers, the premium is an investment in a home that could not exist any other way.

Red Flags for Over-Customizing

Not every customization adds value. Watch for these common traps:

- Overly specific layouts sized for a single piece of furniture or hobby

- Trendy materials that may not age well over the next decade

- Hyper-personalized spaces that are difficult to repurpose at resale

- Premium upgrades in areas buyers rarely notice (e.g., high-end utility room finishes)

A good builder will help you identify which customizations add real value versus resale risk. Semi-custom homes are designed with broad market appeal while still reflecting your personal taste—a balance that tends to perform well when it’s time to sell.

Budget Guardrails: How to Keep Either Path from Blowing Up

Budget overruns rarely happen all at once. They accumulate through small decisions and unclear policies. These guardrails keep your project on track.

Lock These 5 Things Before You Sign

- Complete scope of work, including site prep and utility connections

- All material and finish selections (no open allowances if possible)

- A detailed construction timeline with milestone dates

- A clear change-order policy with defined costs per change

- The full financing structure, including what is and isn’t in the contract price

Preventing Upgrade Creep

Set a firm upgrade budget before selections begin and track every choice against it. Reinbrecht’s approach of presenting curated options with straight costs makes this easier—you see the real price of every upgrade before you commit.

What Contingency Covers (and Doesn’t)

Set aside 5–10% for genuine unknowns: unexpected site conditions, material price spikes, or code changes. According to the NAHB’s 2024 Cost of Construction Survey, construction costs now account for a record 64.4% of the average new home price—making contingency planning more important than ever. This reserve is not meant for mid-build design upgrades; treating it as a slush fund is the fastest way to blow any budget.

Financing Tie-In: Why Build Type Changes Your Loan Strategy

Your choice between semi-custom and custom directly shapes how financing works and how much cash you need during the build.

What Lenders Want to See for Custom

Custom builds require more documentation for construction loan approval. (For a general overview of how construction loans work, the Consumer Financial Protection Bureau offers a helpful primer.) Lenders typically want to review:

- Finalized architectural plans

- A detailed scope of work and builder’s contract

- Proof of permits

- A construction timeline for completion

- Minimum credit score of 680 (most lenders)

- A larger down payment, often 5–20% of total project cost

Draw Schedules, Inspections, and Change Orders

Traditional construction loans disburse funds in “draws” after milestone inspections. Change orders complicate this by altering scope, cost, and timeline—often requiring lender re-approval. This is why custom builds carry higher financing overhead.

Budgeting for Out-of-Pocket Items and Timing

Traditional construction loans require interest-only payments during the build—potentially a year of payments before you move in. Reinbrecht eliminates this with free construction financing up to $250,000. With $1,000 down, that’s your only out-of-pocket expense until closing—available on all loan types (standard mortgage, FHA, VA, or USDA).

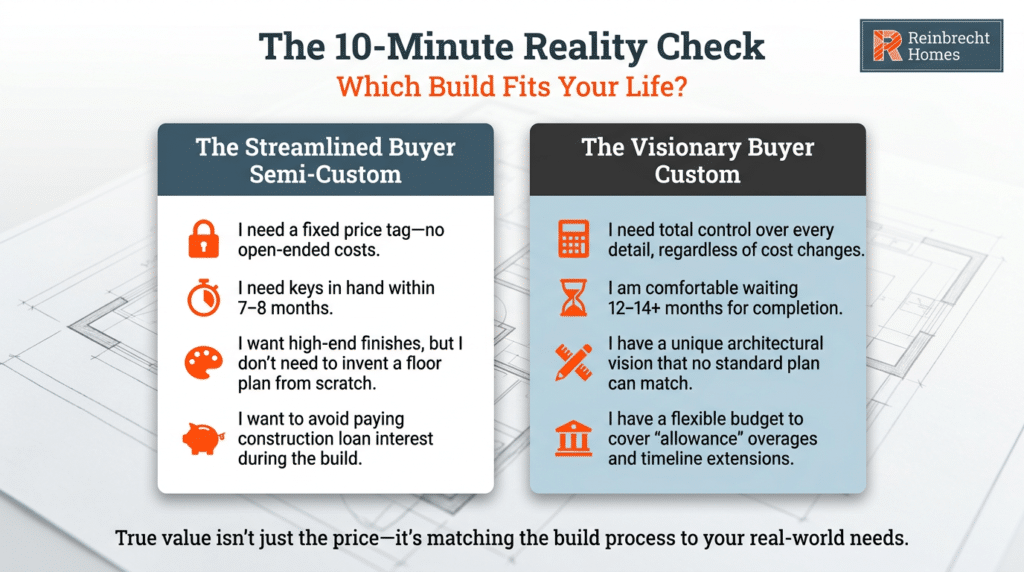

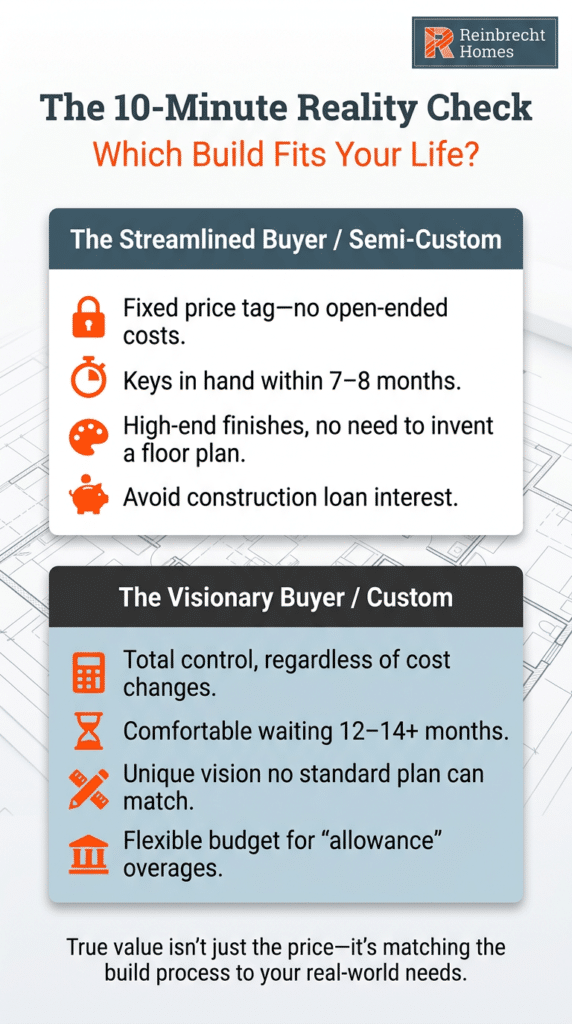

Decision Checklist: Choose Your “Best Value” Path in 10 Minutes

Match your real needs—not your aspirational ones—to the right build type.

Semi-Custom May Be Your Best Value If…

- You want a personalized home but don’t need to design from a blank page

- Budget predictability and a 7–8 month timeline are priorities

- You prefer curated choices over unlimited options

- You want to avoid construction loan interest payments during the build

- Resale value and broad market appeal matter to you

Custom May Be Your Best Value If…

- You have a specific architectural vision no existing plan can accommodate

- Your lot requires a design that can’t be adapted from a standard floor plan

- You’re comfortable with a longer timeline (10–13+ months) and allowance-based budgeting

- You want complete control over every detail and plan to stay long-term

Questions to Ask Your Builder About Pricing Transparency

- Does your contract use fixed pricing or allowances?

- What is included in the base price, and what is not?

- What is your change-order policy and cost per change?

- What financing do you offer, and what are my out-of-pocket costs during construction?

- Can I see a detailed timeline with milestone dates?

Next Step: Build a Financing Plan That Matches Your Build Style

The best way to determine your true budget is to work backward from financing options, not forward from a wish list. Reinbrecht Homes can help you map out a complete financial picture—including construction financing, local banking partners, and a transparent quote that accounts for every dollar before you commit.

Ready to see what your build will actually cost? Schedule a consultation with Reinbrecht Homes to get a detailed, upfront quote. With more than 30 years of experience, over 500 completed homes, and an A+ BBB rating, the Reinbrecht team will walk you through every cost, option, and timeline detail.