If you have searched the cost to build a house in Indiana, you have probably run into some frightening national numbers. Most of those figures come from small national surveys that mix in large custom homes and often leave out the land, so they rarely reflect what a home actually costs to build in Southern Indiana. This guide breaks down where the money really goes, what national averages do and don’t include, and how to get to a number you can plan around.

Key Takeaways

- Construction is the bulk of a new home’s price. NAHB’s 2024 cost survey found construction made up 64.4% of the average new-home sales price, with the finished lot adding another 13.7% on top of it.

- The scary “cost to build” averages come from a small national sample (41 builders in NAHB’s 2024 study) that skews toward large custom homes, so they overstate what a typical Southern Indiana home costs.

- Building and buying cost about the same at the national median. In May 2026 the median new-home price was $424,900 and the median existing-home price was $429,300, a gap of only about $4,400.

- The Midwest is not the automatic bargain many buyers assume. The region including Indiana had a higher custom-home median per square foot ($186) than the national custom median ($166).

- Land cost swings more by town than by anything else in Southern Indiana. Lots start around $45,000 in Reinbrecht’s Newburgh neighborhood and around $19,500 in Princeton, more than double the difference for the same builder.

- Cost per square foot is an unreliable way to compare builders. It hides finish level, site work, and what is or isn’t included in the price, which is why Reinbrecht doesn’t price by the square foot.

- A fixed-price quote with the land and plans included, plus free construction financing up to $250,000 and as little as $1,000 down, turns a scary national range into a predictable local number.

How Much Does It Cost to Build a House in Indiana?

There is no single price to build a house in Indiana, but you can reach a reliable estimate by separating two things that national averages blur together: the cost to construct the home itself, and the all-in price that also includes land, financing, and the builder’s costs. Once you split those apart, the number gets far less intimidating.

National data shows where the money goes. In its 2024 Cost of Constructing a Home study, the National Association of Home Builders (NAHB) broke down the average new single-family home this way:

| Component of a new home’s price | Average (NAHB 2024) | Share of sales price |

|---|---|---|

| Total construction cost | $428,215 | 64.4% |

| Finished lot (the piece most “cost to build” quotes leave out) | $91,057 | 13.7% |

| Builder profit | $72,971 | 11.0% |

| Overhead and general expenses | $38,248 | 5.7% |

| Sales commission | $18,955 | 2.8% |

| Financing | $10,220 | 1.5% |

| Marketing | $5,633 | 0.8% |

| Total sales price | $665,298 | 100% |

Source: NAHB, Cost of Constructing a Home 2024.

One caveat matters more than any single number here. NAHB’s figures come from a small national sample of 41 builders that skews toward larger custom homes, so treat this as a breakdown of where the money goes, not the price to expect in Southern Indiana. A Reinbrecht fixed-price quote includes the land and the architectural plans in the purchase price when you choose one of our floor plans in a Reinbrecht neighborhood, which removes the guesswork about which of these pieces are in or out of your number.

What the National Average Does and Doesn’t Include

Most scary “cost to build” headlines fail on three counts: they rely on a tiny sample, they mix in large custom homes, and they often quote construction only while leaving out the land. Knowing those gaps is the difference between a number that panics you and one you can plan around.

- It is a small national sample. NAHB’s 2024 breakdown rests on 41 usable builder responses, and NAHB itself cautions that the study is not built to represent a typical home.

- It skews toward larger custom homes. The average home in the survey was 2,647 square feet, bigger and more upgraded than most homes built in Southern Indiana, which pulls the averages upward.

- It often leaves out the land. Many “cost to build” quotes describe construction only. In NAHB’s data the finished lot added $91,057, about 13.7% of the total price, on top of construction.

This is the single most useful distinction to hold onto. A construction-only number tells you what the physical home costs to build. An all-in number adds the land, financing, and the builder’s overhead and profit. When you compare quotes or headlines, always ask which one you’re looking at, because the two can differ by six figures.

What Actually Drives Your Cost to Build

Five factors move your number more than anything else: the size and finish level of the home, labor, the land and site work, permits and fees, and how much you customize. National averages flatten all of these into one figure, but your actual cost depends on the choices you make in each category.

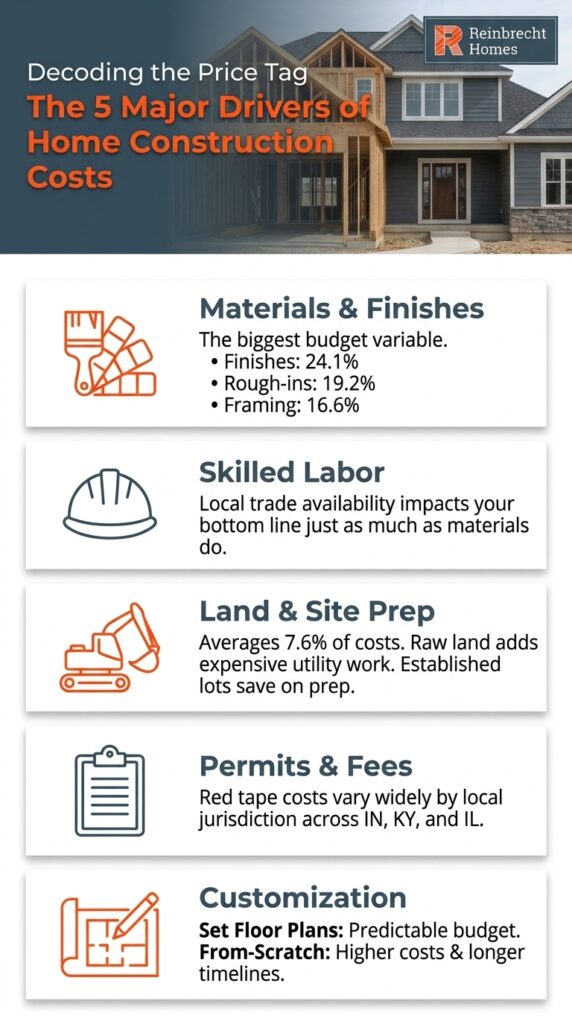

- Materials and finish level: the biggest slice of construction cost is interior finishes at 24.1%, followed by system rough-ins at 19.2% and framing at 16.6%. Cabinets, flooring, countertops, and trim are where budgets swing most, because the same floor plan can be finished simply or lavishly.

- Labor: skilled trade labor is a large and rising share of every build, and local labor availability affects your cost as much as materials do.

- Land and site work: site work averaged 7.6% of construction cost in NAHB’s data, but the real variable is your lot, and it swings by town. Lots start around $45,000 in Reinbrecht’s Hillside Meadows in Newburgh and around $19,500 in Baldwin Estates in Princeton. Building in an established neighborhood usually means the lot is ready with utilities at the street. Building on your own land can mean bringing in infrastructure like electricity, water, and sewage, which adds cost. Reinbrecht can build on the land you already own or place your home in one of its neighborhoods.

- Permits and fees: local permit and impact fees vary by jurisdiction across Southern Indiana, Northwestern Kentucky, and Eastern Illinois.

- Level of customization: the more you move from a set floor plan toward a from-scratch design, the more both the budget and the timeline grow.

Semi-Custom vs. Custom vs. Production: How Your Choice Changes the Budget

The building path you choose is one of the biggest levers on both cost and timeline. Production homes offer the least flexibility at the lowest complexity, full custom offers the most flexibility at the highest cost, and semi-custom sits in the middle: you personalize a proven floor plan without paying to design one from scratch.

- Production homes: built from a fixed set of plans with limited choices. Simple and fast, but little room to personalize.

- Semi-custom homes: you start with one of Reinbrecht’s proven floor plans, then personalize layouts, finishes, fixtures, and upgrades. It’s more personalization than move-in ready and typically simpler and faster than full custom, with pre-construction that usually runs about a month. See how the semi-custom building process works.

- Custom homes: designed from scratch for maximum flexibility. This path carries the highest cost and the longest timeline. Reinbrecht provides a custom home quote typically in less than two weeks, so you still get a firm number early.

Often-Overlooked Costs When You Build

The costs that surprise first-time builders are rarely the big line items. They’re the smaller site and service costs that a low headline number quietly leaves out, plus the difference between an estimate and a fixed price.

- Site work and lot preparation: clearing, grading, and foundation work vary with the lot. NAHB pegged site work at 7.6% of construction cost nationally, and it climbs on difficult sites.

- Utility hookups: on a rural or previously undeveloped lot, bringing in electricity, water, and sewage can add meaningful cost that a neighborhood lot wouldn’t.

- Service and closing-related costs: smaller fees that accumulate around the build rather than in it, and that a bare construction figure ignores.

- Estimate vs. fixed price: an “estimate” or an “allowance” can drift upward as you make selections, while a fixed-price quote locks the number in from the start.

Build vs. Buy in Southern Indiana

At the national level, building and buying cost about the same at the median. In May 2026 the U.S. median new-home price was $424,900 and the median existing-home price was $429,300, a gap of only about $4,400. The “building always costs more” assumption doesn’t hold up at the median.

Locally, the picture varies sharply by submarket, which is why a single citywide median can mislead. Existing homes in Evansville’s urban core sell well below the national median, while the suburban Warrick and northern Vanderburgh County neighborhoods where much of the new construction happens command notably more, according to Indiana Association of REALTORS data. So the real Southern Indiana question is less about a simple price gap and more about trade-offs:

- Buying existing: the fastest way to move in, but you inherit the home’s age, systems, layout, and energy efficiency as they are.

- Building new: you set the layout and finishes, get current energy performance, and start with a fresh warranty. The trade-off is the build timeline. Reinbrecht partners with local banks and supports a full range of home financing and loan options to fit the build.

That trade-off is exactly what one Mt. Carmel, Illinois family weighed. In their words: “We originally planned to remodel a family farm house, but after talking with friends whose homes were built by Reinbrecht Homes, we decided we would be happier with new construction. The Reinbrecht team met with us within a week of our call, started construction within four months, and finished well within the projected completion date!” (Mt. Carmel, IL)

Before you compare paths, it helps to know what you can comfortably afford. Our guide on whether you can afford to build a house walks through debt-to-income, credit, and down payment so you can set a realistic target.

Why Cost Per Square Foot Misleads

Cost per square foot is the metric buyers reach for first and the one that misleads them most. It hides finish level, site conditions, and what a builder includes in the price, so two homes at the same price per square foot can be very different homes.

It also varies by region in ways that defy the “Midwest is cheap” assumption. NAHB’s 2024 data put the custom-home median at $166 per square foot nationally, while the East North Central region that includes Indiana came in higher at $186. A single per-square-foot number can’t tell you whether one builder’s price includes the land, the finishes, and the site work that another’s leaves out. That’s why Reinbrecht doesn’t price by the square foot, and it’s why we wrote a full explainer on why you shouldn’t get hung up on cost per square foot.

How Reinbrecht Keeps Your Number Predictable

The antidote to a scary national range is a number you can actually plan around. Reinbrecht gives you that with transparent, fixed-price quotes: you know the exact cost before you sign anything, with no hidden fees.

- A fixed price, not a moving estimate: your quote is specific and based on what you asked for, so the price doesn’t creep as you make selections. Here’s what goes into a custom homebuilding quote.

- Land and plans included: when you choose one of Reinbrecht’s floor plans in a Reinbrecht neighborhood, the land and architectural plans are already in the purchase price.

- Free construction financing: Reinbrecht offers free construction financing up to $250,000 of the build price, with as little as $1,000 down to start and no interest-only payments during construction.

- Monthly planning: once you have a target price, a mortgage calculator helps you translate it into a monthly payment you’re comfortable with.

That specificity is what customers notice. One Reinbrecht homeowner put it this way: “Our home started with a good plan, then moved on to a budget that included everything from concrete and fill rock to towel bars! The Reinbrecht team helped us make decisions and even took us to the cabinet maker on an icy, winter day. The quotes were specific and based on what we said we wanted. Thanks to everyone who helped us!”

Frequently Asked Questions About the Cost to Build a House in Indiana

What is the average cost to build a house in 2026?

There is no single 2026 average that fits every home, but national data gives useful anchors. NAHB’s 2024 survey put the average new-home sales price at $665,298, of which construction was $428,215 (64.4%) and the finished lot $91,057 (13.7%). That sample skews toward large custom homes, so a typical Southern Indiana build usually costs less.

How much does it cost to build a 2,000-square-foot house?

It depends far more on finishes, site work, and what’s included than on square footage alone, which is why a single per-square-foot price is unreliable. For rough scale, NAHB’s 2024 national custom-home median was $166 per square foot, and the region including Indiana was higher at $186. Use those only as loose context, not a quote, and be wary of comparing builders on price per square foot at all.

Is it cheaper to build a house in Indiana?

Not automatically. The idea that the Midwest is a building bargain doesn’t hold up in the data: the East North Central region that includes Indiana had a higher custom-home median per square foot ($186) than the national custom median ($166) in NAHB’s 2024 figures. What makes a Southern Indiana build affordable isn’t geography alone; it’s controlling your finish level, choosing a proven floor plan, and locking a fixed price.

Why is it so expensive to build a house right now?

Construction costs have climbed to a record share of a new home’s price. NAHB found construction made up 64.4% of the average new-home price in 2024, up from 60.8% in 2022 and the highest since the series began in 1998. Rising materials and skilled-labor costs are the main drivers, which is why your finish selections have such a large effect on the final number.

What are the hidden costs of building a house in Indiana?

The costs that catch buyers off guard are usually site and service costs, not the home itself: utility hookups on undeveloped land, site preparation, and allowances that drift upward as you choose finishes. The best protection is a fixed-price quote that spells out exactly what’s included, so there are no surprises between signing and closing. Reinbrecht’s quotes are transparent and upfront, with the land and plans built into the price when you choose a floor plan in one of its neighborhoods.

Start With a Number You Can Plan Around

The cost to build a house in Indiana is far more predictable than the national headlines suggest, especially when your builder gives you a fixed price with the land and plans included. The next step is turning a general range into a real number for your home. Ready to start planning? Contact the Reinbrecht team to talk through your budget, or explore Reinbrecht’s 30-plus customizable floor plans to find the right starting point.