Building a dream home is a once-in-a-lifetime experience—especially when you can tailor every feature to fit your family’s lifestyle. The homebuilding climate in these regions continues to offer opportunities for new construction, semi-custom designs, and fully custom homes that reflect your unique vision. However, one vital element underpins all these possibilities: arranging the right financing.

This comprehensive guide equips you with a step-by-step plan for financing a custom or semi-custom home. From setting a realistic budget and understanding specialized loan options to preparing your credit and documentation, the process can be navigated confidently with careful planning. Whether you are a first-time homebuyer or a seasoned homeowner, a thorough financial strategy ensures you’ll be well-prepared to break ground on your new home.

By following this checklist, you’ll establish a solid financial foundation for your build, reduce surprises, and ensure that the thrill of designing your dream home remains at the heart of the journey.

The Importance of Preparing for Custom Home Financing

Financing a custom home build is about more than simply getting a loan. It involves coordinating your financial resources with your construction timeline while considering the unique factors that can influence the market.

Reducing Stress and Unexpected Costs

Custom home construction consists of multiple phases—land acquisition, site work, framing, interior finishes, landscaping, and more. Each phase can incur substantial expenses. Preparing a thorough financial strategy and contingency fund helps account for potential price fluctuations in materials or last-minute design changes. This forward-thinking approach saves you from scrambling when the unexpected happens.

Staying on Schedule

In many cases, even a short delay in securing funds can push back construction. If subcontractors or materials are delayed, it could lead to higher labor and storage costs. Proactively sorting out your financing before breaking ground allows you to keep the project moving, avoiding those stressful stop-and-go moments. This is especially critical if you aim to move into your new home by a certain date—such as before the school year begins or to settle into your favorite community promptly.

Understanding Construction Loans and Key Differences

Unlike standard mortgage loans, construction loans are short-term, often requiring interest-only payments during the build. When construction concludes, these loans typically convert to a traditional mortgage. Familiarizing yourself with this structure and any specific local nuances—such as county tax considerations or localized building fees—will help you anticipate and manage costs effectively.

Transparent Collaboration with Your Builder

When your budget is clear from the outset, you can communicate openly with your chosen builder. This transparency sets realistic expectations and ensures that design choices, materials, and timelines align with what you’re prepared to finance.

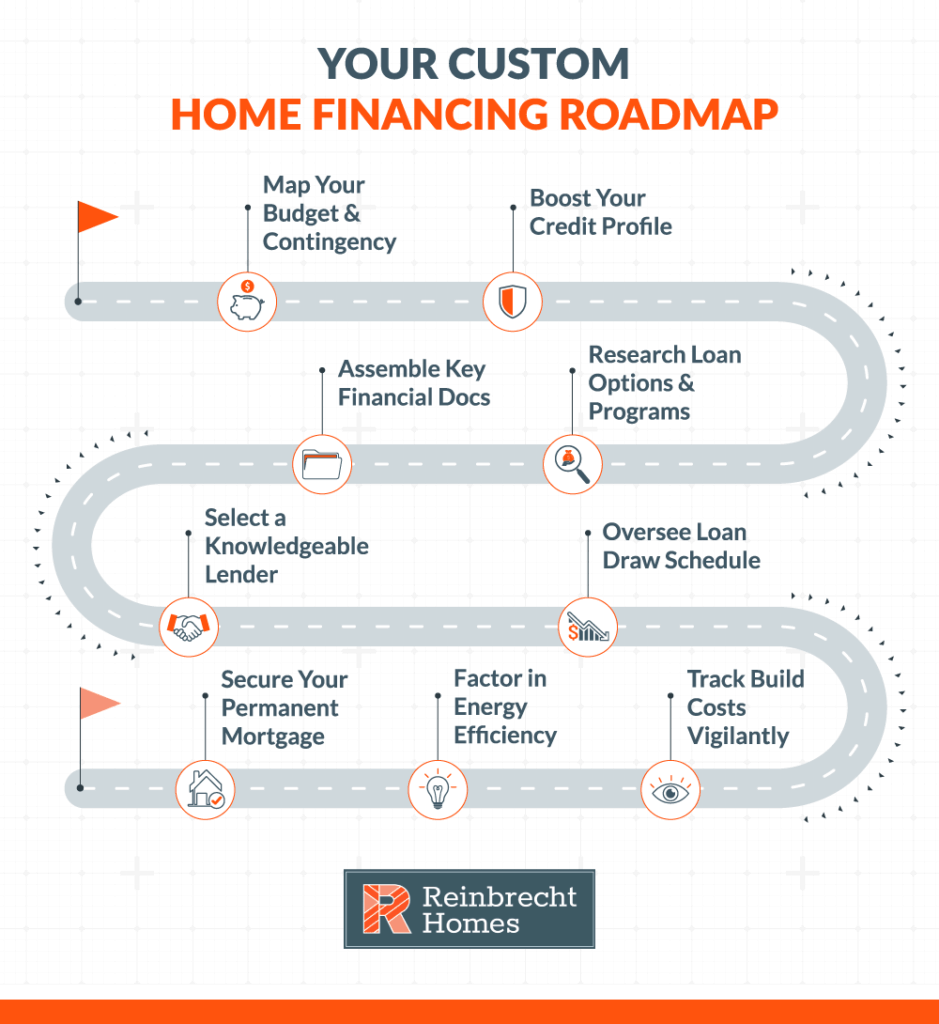

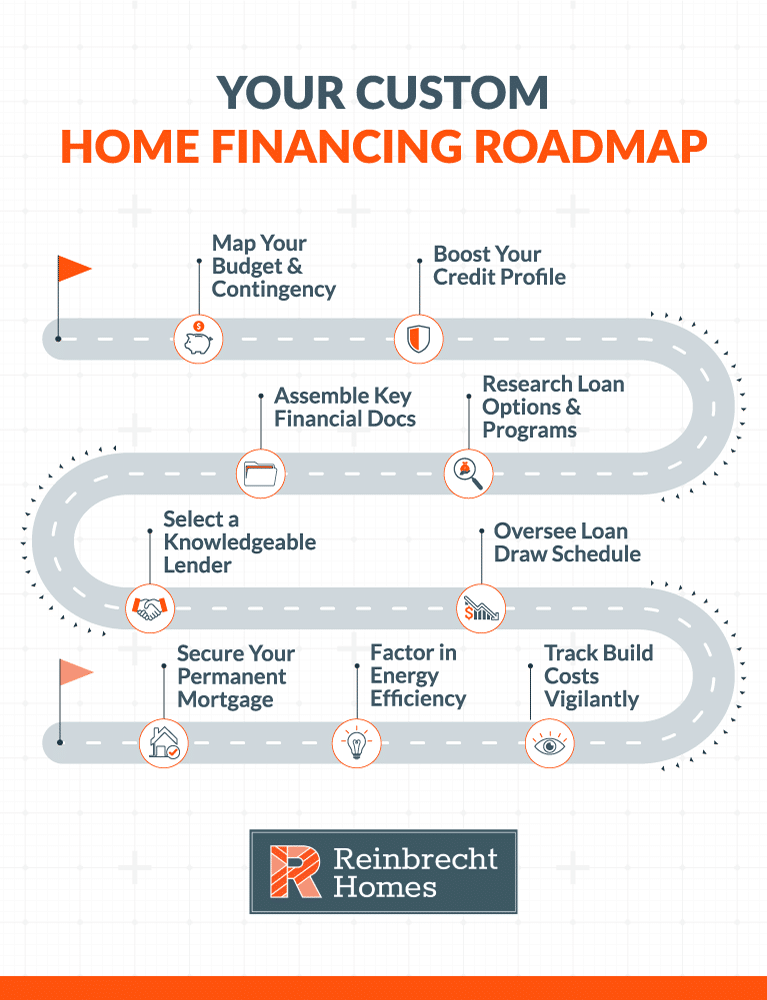

Evaluating Your Budget for a Custom Home Build

Establishing a solid budget is among the most critical steps. This involves aligning your long-term financial goals with the reality of construction, considering everything from land purchase to post-move expenses.

Assess Your Financial Situation

Begin with a clear snapshot of your finances. Evaluate your income, monthly commitments, and projected changes in job status or family size. If you anticipate changes, such as a growing household or relocating to a new area, factor these into your timeline and budget.

Estimate Building Costs

Construction costs can vary significantly based on factors like lot preparation or specialized materials that cater to local climate conditions. Common budget considerations include:

- Land acquisition and site development

- Permits, inspection fees, and utility setup

- Labor, materials, and design upgrades

- Landscaping and driveway installations

- Miscellaneous fees like impact fees or homeowners’ association dues

If you’re unsure about specific design elements, exploring floor plans can give you a concrete reference for potential construction expenses.

Factor in Ongoing and Post-Move Expenses

After you’ve tallied construction costs, remember the ongoing expenses as well:

- Property taxes and homeowners insurance (these can differ notably from county to county)

- Utilities—energy-efficient upgrades can save money long-term

- Maintenance and any local regulations (e.g., specific codes for historical districts in some areas)

Build a Contingency Fund

Build a 5–15% contingency fund into your budget. This buffer allows you to address unplanned changes, including sudden price hikes in materials or modifications to your design plans.

Understanding Financing Options for Custom Home Construction

Knowing the different financing routes is key to selecting the one best suited for your goals.

Construction Loans vs. Traditional Mortgages

While many homebuyers are familiar with 30-year conventional mortgages, construction loans have different terms and higher involvement from lenders during the build. For more details about these distinctions, explore the key differences between a mortgage loan and a construction loan. This resource helps you understand how interest rates, timelines, and documentation requirements vary.

Free Construction Loan Program

Some homebuilders, like Reinbrecht Homes, reduce early financing hurdles for qualified buyers. Prospective homeowners can explore a no-cost construction loan option that eases the initial financial burden and streamlines the process for families building in local areas.

Alternative Financing Methods

If construction loans aren’t the right fit, you might consider personal loans, utilizing the equity in an existing property, or other creative arrangements. Weigh factors such as interest rates, closing costs, and how soon you plan to move into your dream home.

Aligning Payment Structures

Before settling on any single route, discuss the preferred payment schedule with your builder. Some stages of construction—like foundation pouring in certain types of soil or specialized plumbing and electrical installations—must be funded precisely when they begin.

Checking and Improving Your Credit Score

Your credit health is pivotal. An excellent score can unlock lower interest rates, saving you tens of thousands of dollars over the life of your loan.

Review and Correct Your Credit Report

Approximately six months before you secure financing, check your credit via USA.gov. Ensure all your accounts are accurate. If you spot inconsistencies, dispute them promptly to give credit bureaus time to update your report.

Actionable Strategies for Boosting Your Credit

- Limit credit utilization to below 30%.

- Avoid large credit applications in the months before finalizing a construction loan.

- Make payments on time—an automated schedule helps avoid missed deadlines.

- Continue building a positive history by keeping older credit lines open.

A meticulous approach ensures that when lenders assess your profile, you’re poised to secure the most favorable terms possible.

Preparing Necessary Documentation for Financing

Compiling all relevant documents before you start the loan application accelerates the process and shows lenders you’re a serious borrower.

Essential Documents

- Proof of income: recent pay stubs, W-2 forms, and tax returns

- Bank statements (checking, savings, investment accounts)

- Any outstanding debt information (auto loans, credit cards, student loans)

- Government-issued ID and Social Security details

Construction-Specific Documents

- Detailed home plans or construction blueprints

- Cost breakdown estimating labor, materials, and contingencies

- Custom home building timeline highlighting major milestones

- Formal builder contract outlining timelines and costs

- Proof of builder licensing and insurance

Having these assembled in both digital and physical formats can help if you need quick clarifications for your lender.

Choosing the Right Lender for Your Custom Home Build

Identifying a lender with specific experience in custom home construction helps avoid many typical pitfalls.

Key Considerations

- Compare interest rates and origination fees across multiple lenders.

- Evaluate customer service quality—quick communication is often critical when you need funds released on schedule.

- Check local references. Lenders familiar with county-specific requirements can smooth out the permitting and inspection processes.

A trusted lender who understands the regional market makes financing more transparent and adaptable throughout your build.

Managing Financial Commitments During the Building Process

Once construction is underway, maintaining careful oversight of project costs, loan draws, and potential overruns helps you stay on track.

Monitoring Expenses and Disbursements

Many construction loans are doled out in phases corresponding to completed milestones. Stay in close contact with your lender, ensuring draws are released promptly to keep contractors on schedule. If you build with Reinbrecht Homes, you can also track real-time progress through the project tracking tool, Buildertrend, to make sure your financing keeps pace with the construction timeline.

Preparing for Unforeseen Expenses

Even with meticulous planning, modifications in structural design or local code updates can crop up. A well-funded contingency reserve helps avoid project interruptions.

Coordinating Payment Schedules

Plan your loan disbursements to align with critical construction tasks. By setting clear expectations with your builder and lender, you can coordinate labor, materials, and funding to ensure continuous progress.

Emphasizing Transparency

Maintain open dialogue with all parties—especially when changes crystalize mid-project. This fosters a positive environment and helps avoid financial surprises when multiple stakeholders are involved.

The Role of Energy Efficiency in Long-Term Home Affordability

Financing to build a home is a major investment. Ensuring that investment pays off well into the future can be greatly influenced by your home’s energy efficiency.

Investing in Sustainable Features

When building, consider climate-specific approaches to insulation, windows, and HVAC systems. Upfront costs might be higher, but features like LED lighting and advanced insulation techniques generally lower monthly utility bills. Check out insights on how building energy-efficient homes to understand the potential savings.

Incorporating Energy Efficiency in Your Design

From solar-compatible roofs to thermally broken window frames, consult your builder early on about energy-focused add-ons. While these may slightly increase initial loan needs, they enhance comfort and reduce long-term expenses.

Why Finance Your Custom Home With Reinbrecht Homes

No-Cost Construction Loan Option

Reinbrecht Homes partners with lenders to offer a specialized program that helps qualified buyers lighten their financial load early in the process. By streamlining the initial construction loan phase through their financing solutions, they remove hurdles that often cause early delays or unexpected expenses.

Streamlined Communication

Reinbrecht Homes uses Buildertrend’s client portal to keep you informed throughout the build, mitigating any potential finance-related confusion or delays. By providing real-time updates and comprehensive project details, Reinbrecht Homes ensures their clients remain well-informed—reducing the burden of coordinating with individual contractors.

Trusted Local Expertise

Having built homes across Southern Indiana and into Eastern Illinois for over two decades, Reinbrecht Homes understands local regulations, market trends, and the importance of personalizing each build. Their transparent, straightforward guidance ensures you’ll always know where you stand financially. Additionally, their home buyer’s warranty details provide confidence that you remain protected well beyond move-in day.

Final Checklist for Financing a Custom Home Build

Below is a concise list to keep you organized:

1. Define Your Budget Clearly

- Evaluate all construction and post-construction expenses

- Include a contingency fund of at least 5–15% of your total budget

2. Review and Optimize Your Credit

- Check and improve your credit score

- Maintain low credit utilization

3. Explore Financing Options

- Compare construction loans with alternatives

- Ask your builder about special financing programs

4. Gather Your Documentation

- Collect proof of income and bank statements

- Compile detailed cost estimates, plans, and a builder contract

5. Choose an Experienced Lender

- Compare local lenders’ rates and terms

- Prioritize lenders who know regional building requirements

6. Manage Payment Disbursements

- Understand draw schedules and intervals

- Communicate regularly with your lender to avoid holdups

7. Monitor Construction Costs

- Keep a close eye on building expenses

- Tap into contingency funds as necessary

8. Integrate Energy Efficiency

- Weigh up front costs against long-term savings

- Consider climate-specific features for the area

9. Plan for Permanent Financing

- Verify final appraisals

- Confirm the transition from construction loan to mortgage

Future Planning and Market Considerations

As housing demands shift, keep watch on interest rate trends, policy changes, and regional developments or in emerging communities. A minor rate fluctuation or an uptick in property demand can affect material costs and loan availability. Given this, exploring local neighborhood developments ahead of time can help you gauge the potential growth in property values or construction opportunities.

Preparing for Future Refinancing Opportunities

When the construction wraps up, or after you’ve built some home equity, refinancing might be an excellent move. If interest rates drop or your credit score significantly improves, switching to a loan with better terms can cut monthly payments. Speak with your lender well ahead of these transitions to understand the local appraisal process and any closing costs involved.

Maintaining Flexibility and Adapting to Change

Building a custom home is a dynamic process—plans can evolve due to design inspirations, changing family needs, or local market factors. Staying flexible with your financing and taking advantage of new promotions or lower interest rates can enhance your home’s value and keep your finances robust.

Crafting Your Pathway to Building Success

Financing a custom home may seem complex, but with the right approach, it can be a balanced and rewarding experience. By defining a practical budget, safeguarding your credit, organizing documentation, exploring energy-efficient designs, and partnering with credible professionals, you set a strong financial structure that will carry you from foundation to move-in day.

If you’re ready to make your dream home a reality or want personalized guidance on free construction loan options, contact Reinbrecht Homes today to schedule a consultation. With clear communication, expert resources, and a deep understanding of the local market, Reinbrecht Homes can guide you every step of the way—helping your custom home build become a resounding success.