Securing a construction loan can feel overwhelming at first, but understanding the process makes all the difference. Unlike traditional mortgages that finance completed properties, these loans support projects that are still under development. In addition to reviewing your financial health, lenders closely examine your project details and builder qualifications. This comprehensive guide explains what lenders look for and offers clear, actionable advice to help you build a strong, successful application. At Reinbrecht Homes, we understand that home financing can feel like the most intimidating part of building a custom home. That’s why we help clients coordinate key planning details—like budgets, timelines, and documentation—so the construction loan process supports (not slows down) the build.

Why Construction Loan Requirements Differ

Construction loans are unique because they finance homes that have yet to be built. Lenders rely on detailed project plans, future value appraisals (an estimate of your finished home’s worth), and firm timelines to manage the risks involved. Issues such as rising material costs and potential delays demand accurate documentation and realistic planning. By understanding these factors, you can prepare an application that clearly demonstrates your project’s feasibility.

Construction Loans vs. Traditional Mortgages

Construction loans and traditional mortgages serve different purposes. Key distinctions include:

- Incremental Fund Distribution and Shorter Terms: Construction loans release funds gradually as work reaches predefined milestones—such as after completing the foundation or framing. This “incremental distribution” means you receive money in phases rather than as a lump sum. These loans are generally short-term (around 12 months) and often convert into a permanent mortgage once construction is complete.

- Higher Interest Rates Due to Increased Risk: Since the property’s value is based on future estimates, lenders typically charge higher interest rates on construction loans. This increased rate compensates for the additional risk inherent to financing a project that is still underway.

- Appraisal Complexity: Rather than appraising an existing home’s value, lenders estimate the future value based on your plans and comparable projects. This process requires detailed blueprints, comprehensive budgets, and clear project specifications to secure a favorable appraisal.

Why Lenders Scrutinize Construction Loans More Closely

Lenders review these loans with extra care because they involve uncertainties such as rising costs and unexpected delays. They require thorough project plans, clear budgets, and credible builder credentials. This level of scrutiny protects the lender’s investment while ensuring that borrowers have prepared diligently for all potential challenges.

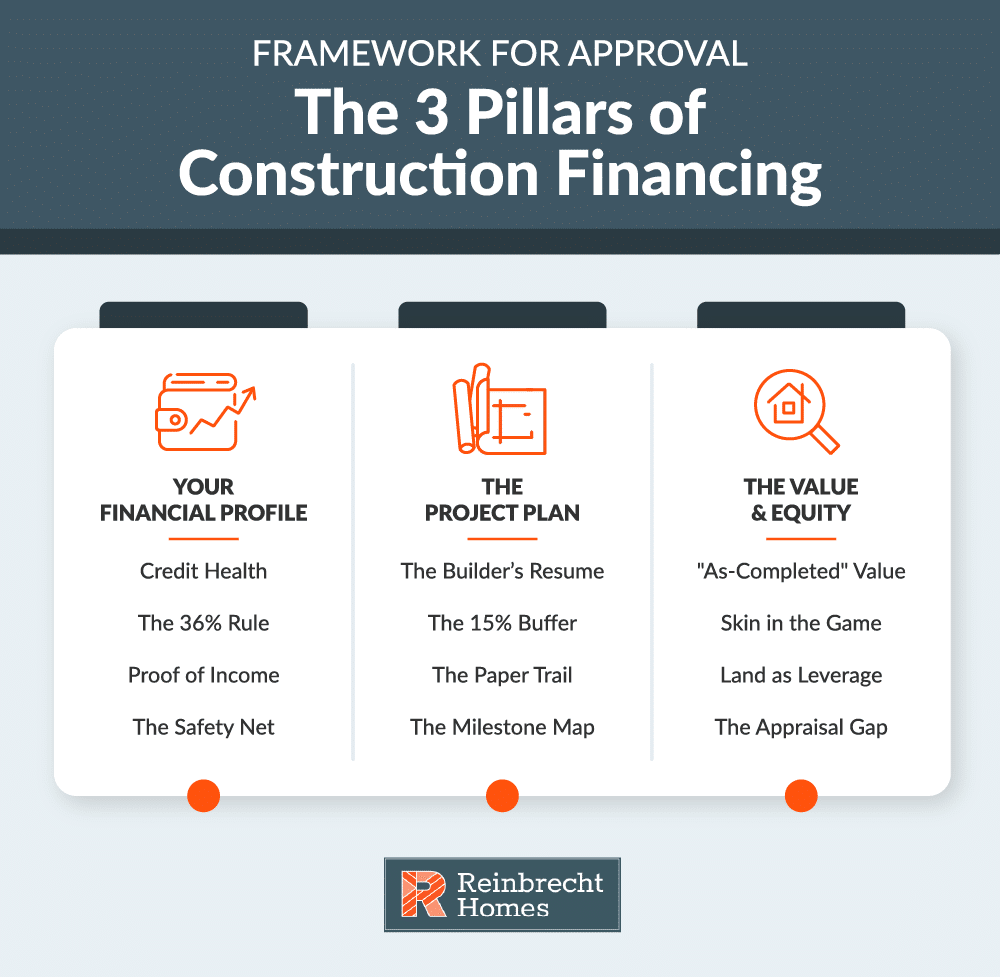

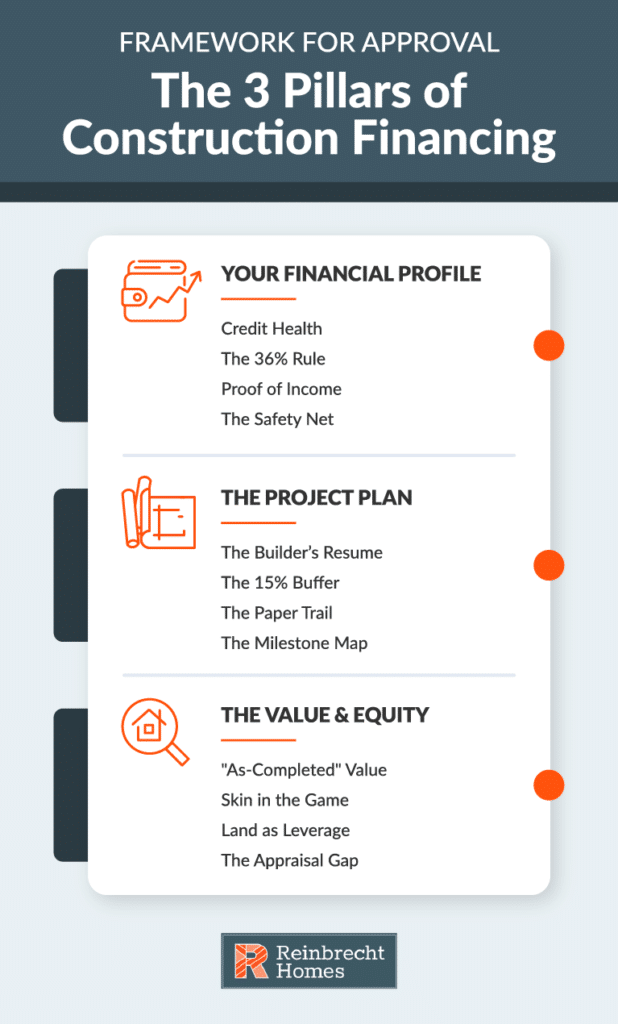

Core Borrower Criteria Lenders Evaluate

Lenders assess both your financial strength and the practicality of your project. Key factors include:

- Credit Score and Credit History: A strong credit score—ideally 700 or higher—and a history of on-time payments indicate that you are a low-risk borrower. If you need a credit boost, consider taking steps to repair your score before applying. For detailed insights on how credit scores are calculated, you can consult the Consumer Financial Protection Bureau.

- Income Stability and Employment History: Lenders look for stable income over the past two years. Providing recent pay stubs, W-2 forms, or tax returns helps demonstrate that you have a reliable income stream to manage loan repayments.

- Debt-to-Income Ratio: Your debt-to-income (DTI) ratio reflects the portion of your monthly income used to service debts. For example, if 35% of your income goes toward debt payments, that is your DTI ratio. Lenders generally prefer ratios around 36% or lower—even though some programs may allow up to 43%. Improving this ratio by reducing debt or boosting income can strengthen your application.

- Cash Reserves and Savings: Having substantial liquid savings reassures lenders that you can handle unexpected expenses. Aim to maintain several months’ worth of payments in reserve, which not only demonstrates financial stability but also reduces perceived risk.

Project-Specific Factors That Matter

A solid, well-organized project plan is as important as your personal financial credentials. Focus on the following:

- Detailed Construction Plans and Specifications: Submit finalized architectural blueprints along with a complete project budget. Clearly break down costs for materials and labor, and include a 10–15% contingency for unforeseen expenses. This attention to detail shows that you have thoroughly planned the project.

- Legal Approvals and Land Ownership: Include proof of land ownership, zoning approvals, and necessary permits. This documentation verifies that the project complies with local regulations and is free from legal issues.

- Builder Credentials and Experience: Lenders prefer working with an experienced, licensed, and insured builder. If you plan to manage the build yourself, be prepared to present extensive documentation to demonstrate your capability.

- Realistic Timelines and Budgets: Provide a clear construction timeline outlining measurable milestones and realistic budgets. A practical schedule, along with a contingency plan for delays or cost overruns, reassures lenders that the project is manageable and likely to be completed as planned.

- Location and Market Conditions: Describe how your project fits within the local market by highlighting neighborhood trends and property values. An understanding of local real estate conditions reinforces lender confidence in the future value of your home.

Down Payment and Equity Expectations

Understanding how much you’ll need to contribute—and how your land or savings can help—sets the stage for a successful construction loan application.

Typical Down Payment Requirements for Construction Loans

Construction loans usually require a larger down payment than a traditional mortgage because the home doesn’t exist yet and the lender is taking on more risk during the build. In many cases, borrowers should expect to contribute 10%–25% of the total project cost (land + construction), depending on credit, income, builder qualifications, and the lender’s guidelines. The more clearly documented and financially conservative your plan is—complete budget, realistic timeline, and a contingency reserve—the easier it is to meet lender requirements without last-minute scrambling.

Using Land Equity as Part of Your Contribution

If you already own the lot (or have owned it long enough for the lender to recognize its value), that equity can often be used to satisfy part—or sometimes most—of your down payment requirement. In simple terms, land equity is the difference between what the land is worth today and what you still owe on it. Lenders typically confirm this through an appraisal and title work, then apply the equity toward your required contribution. This can reduce the cash you need upfront, but it’s still important to budget for closing costs, permits, site prep, and any items your loan may not cover.

How Your Equity Influences Loan Terms and Approval Odds

Equity functions like a risk cushion for the lender. More equity generally improves your position by:

- Lowering the lender’s risk, which can make approval more likely

- Potentially helping you qualify for better pricing or terms (depending on the lender)

- Giving you more flexibility if material costs rise or change orders occur

- Reducing the odds of funding gaps if the appraisal comes in under expectations

Even if a lender doesn’t advertise “better rates for more down,” stronger equity almost always makes your file cleaner and easier to approve—especially when paired with strong credit and documented cash reserves.

Appraisal and “Future Value” Assessments

Before funding your build, lenders want a clear sense of what your finished home will be worth, making the appraisal process a critical step in construction financing.

How Appraisers Estimate the Future Value of a To-Be-Built Home

Unlike a traditional mortgage appraisal, a construction loan appraisal is based on what the home will be worth when finished—often called “future value” or “as-completed value.” Appraisers typically use your plans and documentation to build that estimate, including:

- Final blueprints or construction drawings

- A detailed, itemized budget/spec sheet (materials, finishes, allowances)

- The construction contract and scope of work

- Comparable recent sales of similar homes in the area (size, quality, location)

Because the opinion of value depends heavily on documentation, clean and complete plans—plus realistic selections—can directly influence whether the appraisal supports your loan amount. If you’re curious about the federal guidelines on appraisals and mortgages, the Federal Housing Administration offers helpful documentation.

What Happens if the Appraisal Comes in Low

A low appraisal doesn’t always end the deal, but it does create a gap between the loan amount you want and what the lender is willing to finance. Common outcomes include:

- You bring additional cash to cover the difference

- You revise the plans or selections to reduce total cost (often by adjusting allowances, square footage, or finish levels)

- The builder rebids or reworks the budget to align with market-supported pricing

- You challenge the appraisal (when there are valid errors or stronger comparable sales to support a higher value)

The key is speed and coordination—because appraisal issues often show up late in the process and can derail your timeline if you don’t have a backup plan.

Why Appraisal Gaps Often Kill Construction Loan Approvals

Construction loan approvals depend on the lender’s confidence that the finished home will support the total loan exposure. When the future value comes in too low, it can break the deal for a few reasons:

- The loan no longer meets the lender’s loan-to-value (LTV) requirements

- The borrower may not have enough liquidity to cover the gap plus reserves/closing costs

- The project budget may look inflated compared to neighborhood norms, raising risk concerns

- The lender may view the build as harder to sell if something goes wrong mid-construction

The best way to prevent appraisal gaps is to align the build scope with local market expectations, keep your budget itemized and defensible, and include realistic allowances and a contingency so the numbers hold up under scrutiny.

Essential Documentation Checklist

A complete and well-organized set of documents can greatly improve your application’s credibility. Ensure you have the following:

Personal Financial Documentation

- Recent pay stubs and income verification documents

- Two years of federal tax returns

- Bank statements showing adequate cash reserves

- A current credit report

Construction Project Documentation

- Finalized architectural blueprints and design plans

- A detailed project budget that includes a 10–15% contingency

- Documentation of builder credentials (licenses, insurance, and references)

- Signed contracts outlining work phases and timelines

Property and Land Documentation

- The deed proving land ownership

- Title insurance or clearance documents

- Zoning approvals and building permits

Insurance and Risk Management

- Details of builder’s risk insurance

- Liability insurance certificates

- Any additional coverage required for the project

Organizing these documents logically and clearly will make your application appear professional and thoroughly prepared.

Common Reasons Lenders Decline Construction Loan Applications

Understanding common reasons for loan denial can help you avoid costly mistakes:

- Incomplete or Disorganized Documentation: Missing or poorly arranged paperwork can weaken your application. Make sure every document is complete, clearly labeled, and organized logically.

- Insufficient Credit or High Debt-to-Income Ratio: Weak credit scores or a high DTI ratio signal risk to lenders. Working on improving your credit and reducing debt before applying can strengthen your overall profile.

- Unrealistic Budgets: Underestimating project costs or neglecting to include a contingency fund can lead to funding gaps. Prepare a detailed and realistic budget to avoid surprises during construction.

- Poor Builder Qualifications: Lenders expect you to work with reputable, licensed builders. If you choose to self-build, ensure you have extensive documentation to back up your expertise and planning.

- Land or Permitting Issues: Unresolved land or zoning issues can delay or derail your application. Confirm that all necessary permits and legal requirements are in place before you apply.

- Low Appraisal Estimates: If the estimated future value of your home is lower than expected, the loan amount may be reduced. Ensure your project specifications align with local standards and be ready to modify plans if needed.

- Limited Savings or Financial Instability: Insufficient cash reserves can raise concerns. Building strong savings to cover several months of payments can significantly boost lender confidence.

Steps to Strengthen Your Application

Taking proactive measures can help you secure a construction loan with better terms:

- Prepare Your Finances in Advance: Improve your credit score, reduce existing debt, and build up cash reserves well before you begin your application. Early preparation can lead to more favorable loan terms.

- Partner with Reputable Professionals: Choosing experienced builders and knowledgeable lenders can streamline the process and increase your application’s credibility.

- Develop a Detailed Budget: Work with experts to create a detailed project budget that includes all costs—plus a 10–15% contingency for unforeseen expenses. A realistic and well-planned budget strengthens your case. If you want more guidance on cost projections and budgeting, consider checking Forbes Advisor for best practices.

- Organize Your Documentation: Create a professional application package by meticulously organizing all financial, project, and legal documents. A clear presentation makes a strong impression.

- Maintain Open Communication: Keep in regular contact with your lender and builder. Address any questions or issues promptly to build trust and keep the project on track.

How Financing Fits Into Your Overall Homebuilding Journey

A construction loan is more than a way to fund the build—it’s a planning tool that should align with your overall budget, timeline, and long-term goals for your new home.

Linking Construction Financing to Your Total Home Budget

A construction loan works best when it’s planned as part of your full homebuilding budget—not treated as a separate financial decision. Before construction begins, map out your total costs, including land (if applicable), site prep, permits, utilities, design selections, and a contingency reserve for overruns. Then compare that complete budget to your approved loan amount and cash contribution so you have a clear picture of what’s covered, what’s out-of-pocket, and where you may need to adjust selections to stay aligned with your financial goals.

Coordinating Your Loan Timeline With Design and Build Milestones

Construction loans typically fund your project in stages, so it’s important to align your loan draw schedule with key construction checkpoints. Work with your builder and lender to confirm how and when funds will be released—for example, after foundation completion, framing, mechanical rough-ins, and final finishes. This coordination helps avoid delays caused by funding gaps, keeps subcontractors and materials on schedule, and gives you a structured way to monitor progress and approvals as the build moves forward.

Resources and Next Steps

To keep momentum and reduce surprises, gather the documents and contacts you’ll need early and set clear communication expectations with your builder and lender. Helpful next steps include:

- Review your full project budget and confirm your contingency plan.

- Verify your projected construction timeline and draw schedule with your lender.

- Create a simple tracking system for invoices, inspections, and change orders.

- Clarify how the construction loan will transition into your permanent mortgage.

Build With Confidence From Application to Move-In Day

Securing a construction loan is a vital step toward creating your dream home. By addressing both your financial profile and the feasibility of your project, you can overcome common challenges and present a strong, complete application. Start by reviewing your finances, finalizing your construction plans, and consulting with trusted professionals. When you’re ready to take the next step, the Reinbrecht Homes team can help you turn early planning into a build-ready roadmap—so your lender, your builder, and your budget stay aligned from start to finish. Contact us today to take control of your construction journey and move one step closer to building the home you’ve always envisioned.